Industry Categorization

2

Rite Aid Corporation belongs to the drug retail sub-industry, which ladders up into the food and staples retailing industry/industry group. These are all part of the consumer staples sector.

2/18

Industrial Comparison - Profitability (2020)

4

As expected, most sectors of the economy suffered in terms of profitability in 2020 due to the COVID-19 pandemic. However, some industries were still able to turn a profit in the tumultuous year. These include the Utilities, Real Estate, and Financial sectors. This makes sense, especially for the utilities sector, as the demand for water and power did not cease in the US - if anything, it increased, as millions of Americans stayed isolated at home. In fact, 90% of all firms in this sector were profitable in 2020. Regarding real estate, millions of people moved out of expensive cities and into other parts of the country in order to work remotely. This caused an uptick in real estate transactions and prices (and therefore profit margins).The very high median revenue within the utilities sector also indicates a more monopolistic environment, while it is clear that the financial sector is a bit more diversified and competitive.

The consumer staples sector has an average total revenue, median operating margin, and median revenue - indicating average performance with a diverse/competitive landscape.

4/18

Industrial Comparison - Growth (2020)

5

As expected, the COVID-19 pandemic and subsequent shutdown of the country absolutely devastated businesses across all sectors and industries. Unlike home utilities, which saw decent profitability statistics (previous slide), we clearly see here that the energy sector experienced tremendous shrinkage in terms of net income growth and income/revenue growth rates in 2020. Revenue growth for the sector was not as bad, but as we learned in class, just because revenue is high does not mean that the net income or profits of the firms will also be high, as their expenditures can far outweigh the money brought in.

Consumer staples fared better than most other sectors in 2020, having a slightly positive total operating income and net income growth rates in addition to stronger than average median revenue, income, and net income growth rates. The only other sector that came somewhat close was the financial sector.

5/18

Industrial Comparison - Efficiency (2020)

6

The industry comparison for efficiency shows a very similar picture when compared to previous years. The healthcare sector has by far the highest median sales general admin cost/total revenue ratio, complementing the bar graphs on the right showing that the median return on assets and invested capital is very much in the negative. This makes sense, as the pharmaceutical industry's investments in research and development are very high compared to other industries.

For the consumer staples sector, we can see that the median inventory turnover and productivity are on par with other sectors, meaning that this sector has similar inventory turnover to the telecom, materials, industrials, and IT sectors. The median labor productivity is understandably lower than the energy and real estate sectors, as those sectors typically make high profits with relatively few employees (it only takes a few individuals at a time to sell a property while it takes hundreds/thousands of highly paid specialists to bring a new drug to market).

6/18

Industrial Comparison - Profitability (2020)

8

Compared to 2019, there was not much of a difference across the entire industry in terms of revenue, income, and profit margins. Total revenue was highest with hypermarkets and supercenters, as well as with drug retail (aka retail pharmacies). It should be noted that the median revenue was high with both drug retail and hypermarkets and supercenters, meaning that those markets are less competitive and more monopolistic in nature. In the US, for example, there are only a few retail pharmacy chains that are considered to be very large. Smaller competitors, such as independent pharmacies, typically get outcompeted and are squeezed out by the very low insurance reimbursements for medications, as well as high cost of goods for over the counter products. Larger drug retailers are able to maintain a razor thin profit margin by negotiating optimal rates with PBMs and drug suppliers. Smaller companies do not have that negotiating power and are thus forced out of the competition. This issue is becoming increasingly worse with the passing years and the pandemic has accelerated that. It is likely that the ~70% of drug retailers that are profitable (according to the bottom right graph) are larger companies and the roughly 30% that are unprofitable are smaller ones that simply cannot get a large enough foothold to compete with the big players.

8/18

Industrial Comparison - Growth (2020)

9

We were surprised to see that the the operating and net income growth rates were negative for the drug retail sub-industry. The onset of the pandemic drew unprecedented demand for basic goods that are sold by pharmacy retailers, including over the counter drugs. In fact, some drug manufacturers saw record profit growth during 2020 in their over the counter divisions due to this demand. The fact that this did not translate into an increased income growth rate for retailers is interesting. As in 2019, food distributors saw the greatest decrease in operating and net income growth rates, though they have accelerated in 2020 due to the pandemic. One possible explanation for this is that the distributors were under pressure to maintain their pricing for supermarkets (and ultimately consumers) while themselves struggling with supply chain issues, leading to them sourcing food products from more expensive suppliers and driving up their own expenses.

9/18

Industrial Comparison - Efficiency (2020)

10

The median return on assets and on invested capital are quite low for the retail drug sub-industry. In fact, it is the lowest in the industry, other than for food distributors. That is not entirely surprising, though, as drug retailers are known to have a very small margin on the items they sell. They have a substantial amount of expenses (purchase of over the counter goods, purchase of drugs) and are not reimbursed much for sales of prescription drugs (profits can be as little as $0.25 per prescription). Simultaneously, they cannot price their goods much higher than they do because supercenter retailers such as Walmart or Target offer much lower prices on the same goods, and there will come a point (if the prices are raised high enough) that consumers will forego the convenience of picking their goods up at the pharmacy and instead patronize a larger big box retailer, leading to huge profit losses for the pharmacy chains. Overall, however, inventory turnover remains very high among drug retailers, as does labor productivity. It is clear that the pandemic did not affect the drug retail sub-industry as much as some others due to unwavering demand due to the nature of their business/products.

10/18

Industrial Breakdown - Revenue (2020)

12

This is a breakdown of the revenue of the drug retailer sub-industry in the US. A very large portion of revenue goes towards purchasing inventory/goods, which includes over the counter drugs and merchandise and prescription medications (which are very expensive, despite the wholesale discounts). It makes sense that COGs takes up such a large amount of the revenue. SG&A expenses, which include things like salaries, executive bonuses, store rent, etc., account for over 7% of the revenue amount. Only about 1.75% of the total revenue is pure profit or the net income. Thus, it is clear that drug retail companies operate on a razor thin margin. The previous (prepandemic) year, 2019, did not see much greater net revenue, at only 2.45% of total revenue. This small margin will become more apparent with subsequent analyses on the last slide of this section.

12/18

Concentration and Competition Intensity - Total Revenue

13

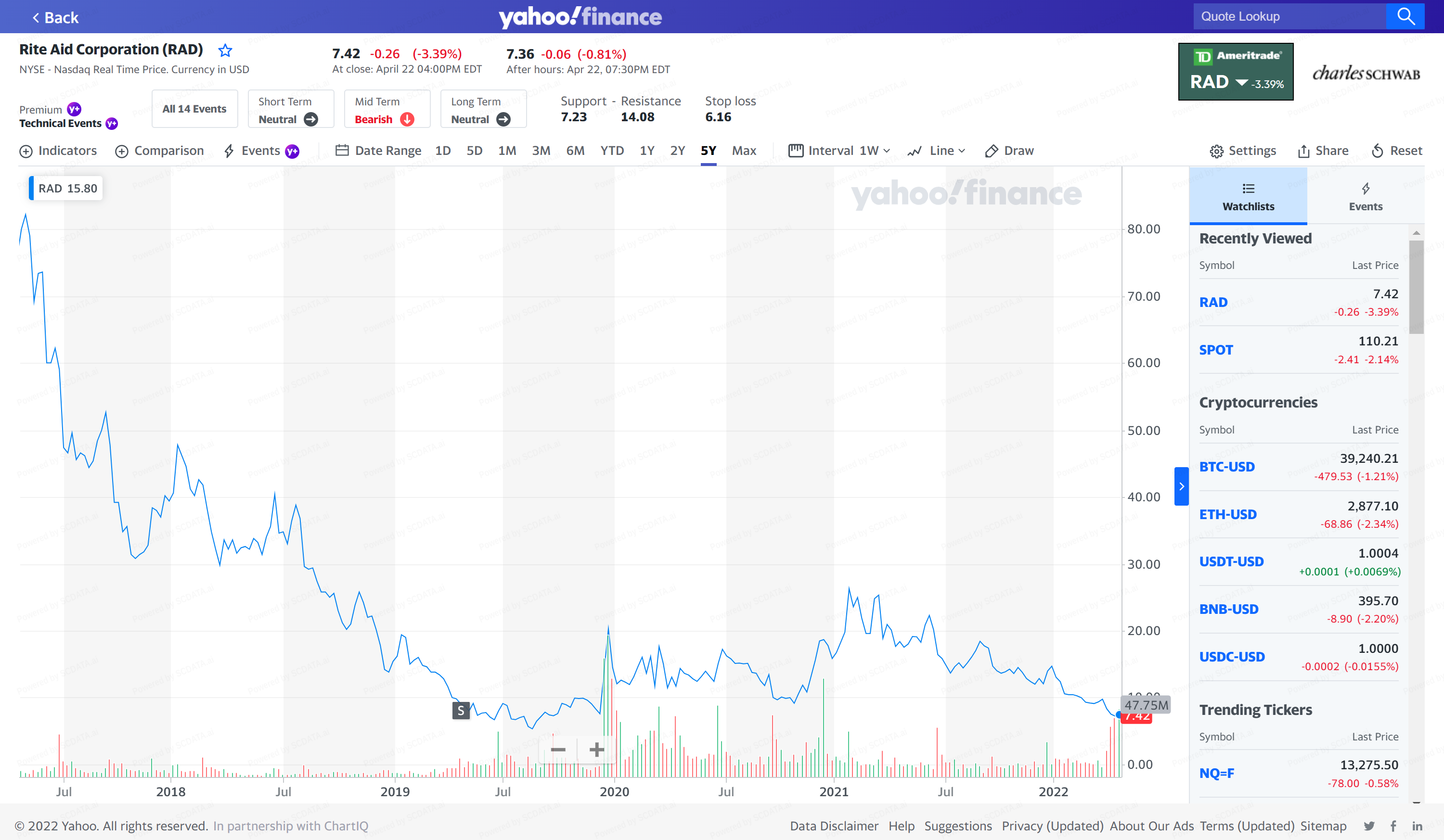

As predicted by the previous median revenue data in the industry, it is clear that the drug retail sub-industry in the US is very monopolistic. It is completely dominated by only a few retail giants - CVS, Walgreens, and Rite Aid (our company of focus). As we can see, Rite Aid's total share of revenue has considerably decreased since the mid-2010s, while CVS's (the largest company in terms of total revenue) has increased. It is interesting to note that, while Walgreens purchased over 1900 Rite Aid locations in a multibillion dollar deal in 2018, Rite Aid's total revenue share has not severely decreased (and Walgreens's has not significantly increased). This indicates that there have been additional changes made to the Rite Aid business. Upon further research, it became apparent that Rite Aid is attempting to brand itself as a wellness/natural-based retail destination. This is evident by the new Rite Aid logo, depicting a more natural or holistic approach to medicine, as well as the addition of a substantial number of natural products that appeal to a certain demographic of consumers. It could be said that Rite Aid has done a fairly decent job at differentiating itself from the other mainstream chains in that way. Additionally, the chain is known for their great customer service, meaning it has a loyal following of customers that continue to help the company turn a profit.

13/18

Concentration and Competition Intensity - Operating Income or Loss

14

The operating income paints an even more grim picture for some of the smaller large drug retailers. While CVS Health has managed to hold on to a fairly large operating income, which was only slightly smaller than 2019 and on par with 2015 and 2017, the operating income for both Walgreens and Rite Aid have decreased to virtually nothing. In fact, Walgreens's operating income decreased a staggering 73.7% to only $1.3 billion in 2020.

This phenomenon is likely due to how well CVS Health has diversified in recent years prior to the pandemic. CVS Health owns both Aetna, a health insurance giant, as well as CVS Caremark, a large pharmacy benefits manager dealing specifically with prescription drug coverage. The diversity of CVS's portfolio allowed the company to still turn a decent profit overall even though some parts of the business were hurting. Walgreens and Rite Aid, on the other hand, have not diversified as much - their investments are still largely on the retail pharmacy space. While OTC and prescription drugs have continued to be in demand through 2020, sales of other merchandise in the stores (seasonal items, back to school items, travel items, makeup, etc.) have suffered greatly. They were simply not as well-positioned to weather the storm of the COVID-19 pandemic. In general, Rite Aid has been struggling for several years to generate a substantial profit. Operating costs for some initiatives (Plenti rewards program) that were not profitable were quite high, which likely drove the operating income down for the company. While other drug retailers owned drug suppliers, insurance companies, and PBMs, Rite Aid had virtually none of that. The chain has had a hard time keeping up with the other giants, which have slowly but surely been forcing Rite Aid out of the scene. Cutting operating expenses (which they have been doing) does not seem to be working as operating income has been trending downwards along with total revenue.

14/18

Industrial Trend - Industry Total Size

15

Even before the pandemic, we can see that there has been a clear, ongoing trend where (despite growing total revenue and steady operating income) there are fewer and fewer companies that are considered to be profitable. Due to the entire industry being dominated by just a handful of companies in the US, there is not much more room for them to grow within their traditional settings. Virtually all of the market share has already been eaten up - thus companies are left with the options of improving the user/consumer experience (streamlined apps, better in-store/online offerings, etc.), diversifying into other sectors and industries (healthcare services), or simply doing nothing and losing market share to the competition. As a response to CVS's highly successful diversification into the healthcare services industry with its Minute Clinic, Walgreens has been rolling out its Walgreens Community Clinics to some of its locations. However, the initiative has failed to rival CVS's, and as of now these clinics are available at only 400+ stores out of the 1000s of Walgreens nationwide. Minute Clinic, meanwhile, has more than triple the number of locations in over half the US states. CVS simply has much better penetration.

Rite Aid, meanwhile, has no robust nationwide clinic program and has had a rocky few years. The failed mergers with both Walgreens and Albertsons also made investors wary of putting money into the clearly struggling business. With waning hope of a rescue buyout from another drug retailer, investors have continued to steadily pull their funds out of Rite Aid stock - since it was now apparent that the company was unable to make itself competitive again with new initiatives, cost-cutting, or diversification - leading to a drastic decrease in stock price. In fact, Rite Aid performed a 1-for-20 reverse stock split in 2019 in order to avoid being removed from the NYSE because of their low share price (which was under $1 by that point).

15/18

Enterprise Trend - Profitability

16

These graphs indicate the presence of operating inefficiencies in both Walgreens and Rite Aid. CVS - despite having the lowest gross margin among the three companies, maintains the largest operating margin by a significant amount, especially in 2020. This shows that, despite a smaller margin on sales, the company efficiently manages its operating costs/expenses. It thus makes sense that Rite Aid, which has been plagued by inefficient management, resource allocation, and high debt has a negative net margin and negative return on assets, despite improved performance in those parameters in 2020.

16/18

{kind=link}

{kind=link}